The European Central Bank is anticipated to keep its deposit rate unchanged at its April 30 meeting before implementing an increase in June, according to a majority of economists surveyed by Reuters. The move would aim to combat inflation pressures stemming from energy price spikes related to ongoing Middle East warfare.

While most analysts agree on the June timing, there’s significant disagreement about subsequent policy moves, with the quarter-point increase viewed primarily as a precautionary measure given uncertainty around broader inflationary impacts from elevated fuel costs.

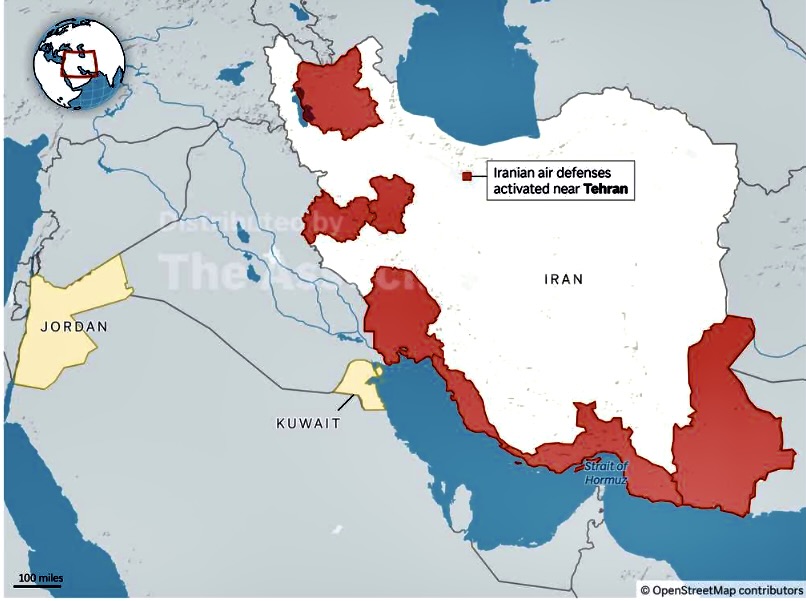

Nearly two months of Middle East conflict have driven oil prices higher, pushing inflation significantly above the ECB’s 2% goal and prompting financial markets to anticipate multiple rate hikes this year while weakening business and consumer confidence.

Although ECB officials have expressed stronger anti-inflation resolve compared to other central banks, they’ve downplayed prospects for immediate rate action, stating insufficient evidence that energy price increases—beyond their direct control—are spreading to other sectors.

The institution remains influenced by its delayed response to 2022’s rapid inflation surge, while also seeking to avoid repeating its 2011 error when two rate increases over four months during rising commodity prices worsened the eurozone debt crisis.

Nearly all 85 economists polled between April 17-23 predicted the ECB would maintain its 2% deposit rate next week. Of those surveyed, 44 forecasted a June bump to 2.25%, while 40 expected no adjustment. Most economists had previously anticipated unchanged rates throughout this year until recent weeks.

“The ECB will try to avoid a repeat of 2011. They need to have some clarity that whenever they hike, they’re not going to have to undo that quickly. And that’s a reason to move in June rather than in April,” said Ruben Segura-Cayuela, Bank of America’s head of European economics research.

“There’s still a scenario in which the ECB looks through the shock… The risk is the activity will react a bit more negatively than we are expecting. That might create additional incentives to delay hikes. And once you delay hikes, at some point, you might decide not to hike at all,” he added.

Economists showed no agreement on policy direction after June, with 34 of 85 expecting at least one additional increase before year-end.

“The ECB doesn’t have the luxury to wait for the second-round effects to show up in the data. If they do see it in the data, it’s already too late. And that’s why we think they will deliver two interest rate hikes in June and September out of precautionary and forward-looking considerations,” stated Anna Titareva, UBS European economist.

More than 40% of respondents—35 of 85—still anticipate no rate modifications this year.

“I think right now, if oil stays around the $100 mark, it will give the ECB cover to just sort of sit back and watch inflation expectations… as long as they’re not getting out of control, that’s valid reason enough for the ECB to stay on the sidelines,” explained Jennifer Lee, BMO Capital Markets senior economist.

Brent crude has maintained an average near $100 per barrel this month, surpassing the ECB’s March baseline projection of a $90 peak, though remaining below the $119 worst-case scenario.

Inflation, which rose to 2.6% last month from February’s 1.9%, is now projected to average slightly above 3% over the coming three quarters and 2.7% annually, aligning closely with ECB forecasts.

Quarterly economic expansion is expected to hover around 0.2% throughout the year, producing 0.9% growth in 2026, down from the 1.2% predicted in early March.

The region’s two largest economies, Germany and France, are projected to grow 0.7% and 0.9% respectively this year, representing modest downgrades from January survey results.