WASHINGTON – International finance officials gathered in the nation’s capital this week found themselves confronting a harsh reality: their capacity to shield the global economy from mounting geopolitical crises remains severely constrained.

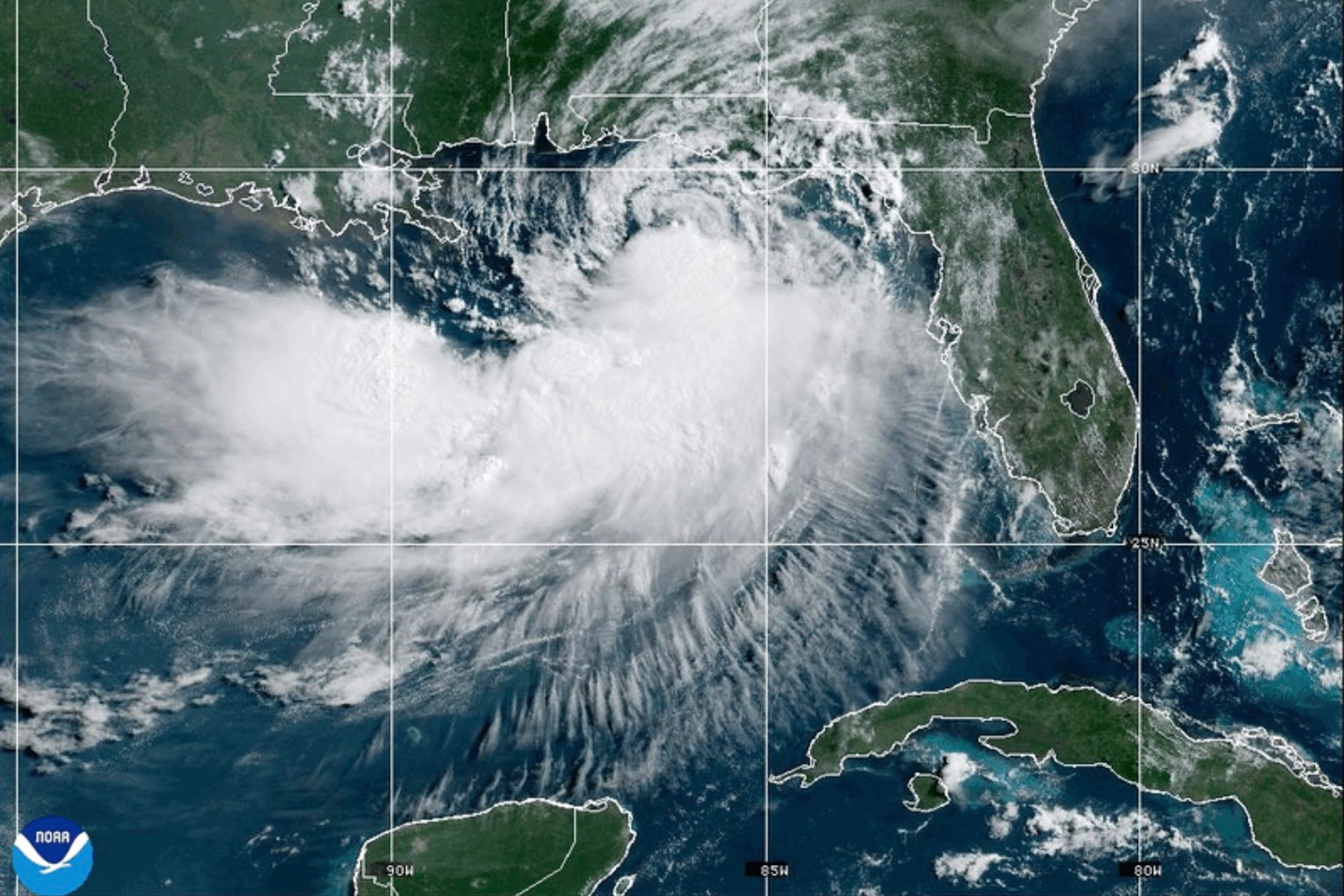

During the International Monetary Fund and World Bank Spring Meetings, delegates experienced dramatic mood swings as Middle East conflict developments alternately darkened and brightened economic prospects. Initial pessimism about worsening global conditions due to energy supply disruptions gave way to cautious hope when Iran appeared ready to reopen the Strait of Hormuz for commodity shipments. However, fresh shipping attacks by Saturday had already dampened that brief optimism.

The financial institutions announced a joint commitment of up to $150 billion in new assistance for developing nations most severely affected by energy price volatility. They also marked their return to engagement with Venezuela’s acting administration following a seven-year hiatus.

Officials urged nations against stockpiling oil reserves and implementing costly, broad fuel subsidies. Yet ultimately, their influence proved limited as they monitored diplomatic exchanges between Tehran and Washington.

Josh Lipsky, who chairs international economics at the Atlantic Council, observed the constraints facing these institutions. “Actually some of the most important decisions on the global economy are not happening here,” Lipsky noted regarding the IMF and World Bank headquarters.

“The single most important development in the global economy happened between the U.S. and Iran,” he continued. “We hope it’s good news, and we’ll wait and see.”

Saudi Finance Minister Mohammed Al-Jadaan captured widespread official sentiment despite rising stock markets and declining oil futures Friday. He emphasized his reluctance to forecast improvement until commercial vessels resume normal transit through the strait with affordable insurance coverage and energy costs decline.

“If the clear waters are open,” Al-Jadaan stated during a press briefing, “I think that’s what would trigger, for me, a change in the scenario.”

The IMF’s modest reduction of global growth projections to 3.1% for 2026 under its most favorable scenario quickly became obsolete, with the organization indicating the economy was trending toward a more pessimistic 2.5% growth rate. Their latest World Economic Outlook warned that extended conflict could drive the global economy into recession.

The current crisis emerged as the world economy was still recovering from previous disruptions, including President Donald Trump’s significant tariff increases on international trading partners implemented late last year.

Trade dispute discussions received less attention at this year’s gatherings, as did Russia’s ongoing conflict in Ukraine, though G7 finance ministers committed to maintaining pressure on Moscow.

The continuous series of economic disruptions beginning with the COVID-19 pandemic in 2020 and Russia’s Ukraine invasion in 2022 has demonstrated that the United States no longer serves as “the general” of international order and may not provide crisis solutions, according to Lipsky.

Treasury Secretary Scott Bessent announced Friday a new initiative encouraging G20 nations, the IMF, and World Bank to coordinate ensuring fertilizer access amid Gulf supply interruptions. However, seven weeks into the conflict, this effort offers little relief for farmers currently planting spring crops across the Northern Hemisphere facing shortages and elevated prices.

African Development Bank Chief Economist Kevin Chika Urama said the Middle East crisis reinforced the need for African nations to strengthen regional commerce and economic connections, develop alternative energy sources, expand domestic revenue collection, and utilize substantial natural gas deposits.

“Geopolitical tensions are the new normal and uncertainty in policymaking has become certain,” he told a panel of multilateral institution economists.

Finance ministers, central bankers, and other attendees expressed frustration at being drawn into another economic crisis by Trump’s decisions.

In private discussions, officials, particularly Europeans, clearly communicated to the U.S. that Washington must act to reopen the strait, according to a senior finance official present at the meetings. Public statements remained more diplomatic with reduced blame assignment.

“The knot of this conflict is the Strait of Hormuz. We need this to open, but not at any price,” French Finance Minister Roland Lescure told media representatives. “I don’t want to pay a dollar to go through the Strait of Hormuz.”

Consecutive crises, including the current war, have disrupted developing economy planning “and you hardly have time to breathe,” said Retselisitsoe Adelaide Matlanyane, Lesotho’s Minister of Finance and Development Planning, during an African ministers’ panel.

“For small, open, and vulnerable economies like Lesotho, these shocks have presented extraordinary pressures on the fiscals, on prices and on everything.”

Matlanyane explained that debt management has become increasingly complex and tensions have “brought on a sense that we have to rethink policy and we have to think differently.”

“It’s frustrating dealing with this,” she told reporters.

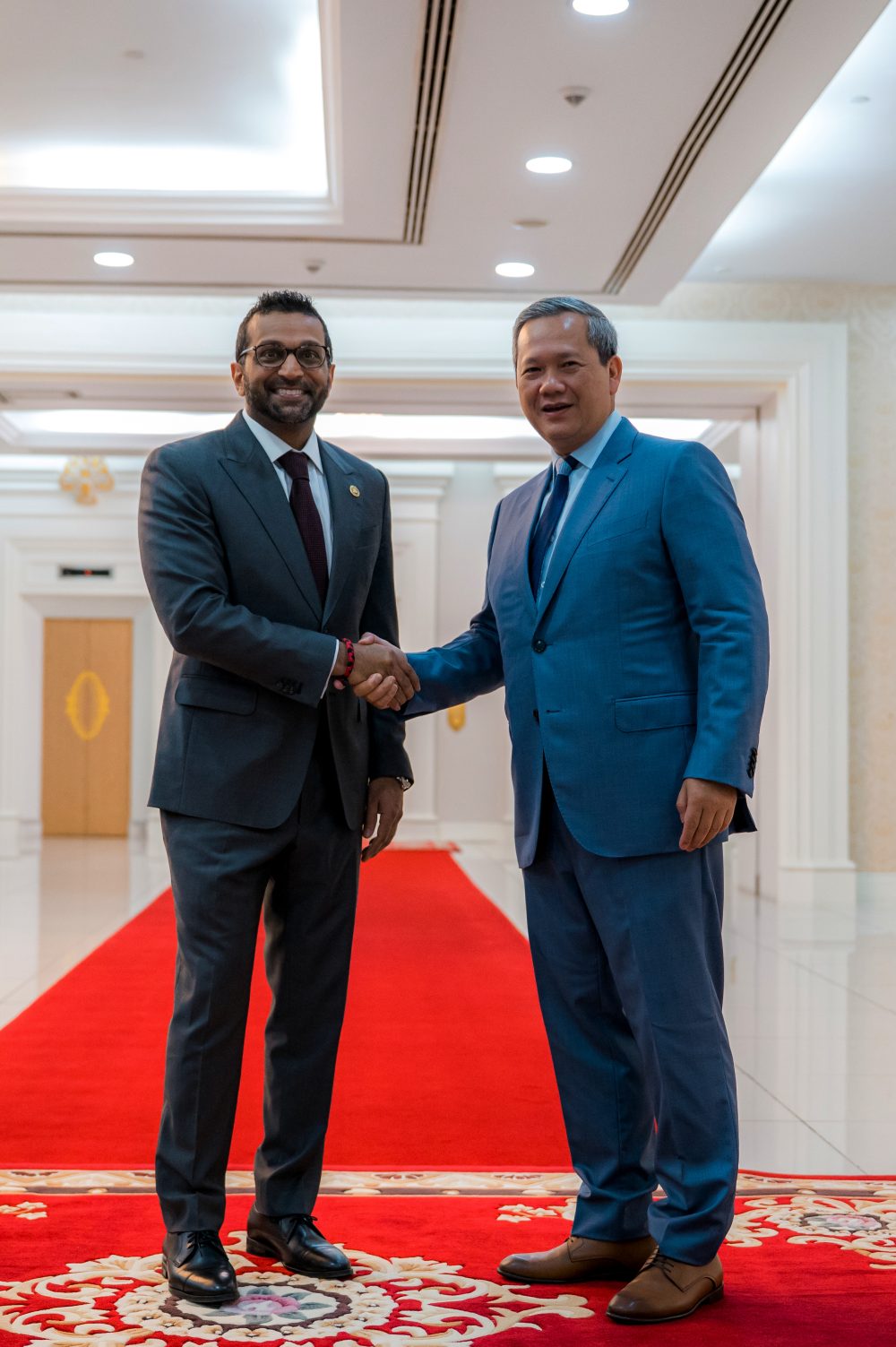

For Thailand, an energy-importing nation scheduled to host October’s IMF and World Bank annual meetings, lasting effects from damaged Gulf energy infrastructure will maintain elevated prices long-term, said Deputy Prime Minister Ekniti Nitithanprapas.

However, he viewed the crisis as an opportunity for Thailand to decrease fossil fuel dependence and expand renewable energy, including solar installations – contrasting with Trump’s energy policies.

“We need to commit to transform…to help people transform to face the new fragmented world and high oil prices,” Nitithanprapas stated.