(Editor’s note: John Hall is a professional commodities analyst.)

Agricultural economists presenting at the Ag Forum Outlook conference on Feb. 19-20 announced their findings: “The U.S. corn outlook for 2026-27 is for reduced production, domestic use, exports and ending stocks.”

Forecasters anticipate the corn harvest will reach 15.8 billion bushels, representing approximately a 7 percent decrease compared to the previous year’s production.

Farmers are expected to plant corn on 94.0 million acres, a reduction of 4.8 million acres from last year’s totals. Yield estimates of 183.0 bushels per acre are based on assumptions of typical planting schedules and average summer weather conditions.

Despite higher beginning inventory levels from the previous season, total corn supplies are predicted to reach 17.9 billion bushels, down from the record 18.6 billion bushels recorded in 2025-26.

The situation involves multiple declining factors: fewer planted acres, reduced production, and decreased usage, combined with substantial carryover inventory from the prior year.

Overall U.S. corn consumption for 2026-27 is expected to drop roughly 2 percent due to lower domestic demand and reduced export volumes.

Food, seed, and industrial consumption remains steady at 7 billion bushels. Ethanol production is projected to utilize 5.6 billion bushels, reflecting expectations of stable gasoline consumption and export levels.

Feed and residual usage is anticipated to decline about 3 percent to 6 billion bushels based on reduced supply availability.

Export volumes are forecast to decrease by 200 million bushels to 3.1 billion.

America’s share of global corn trade is expected to shrink slightly as South American competitors increase their exports and worldwide demand growth remains modest.

The global corn landscape has undergone dramatic transformation!

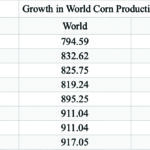

Here’s the broader context. In my Feb. 17 analysis, I examined worldwide corn production patterns. The data revealed a clear trend using 2017-18 as the baseline year.

Evidence clearly demonstrates that global corn expansion began accelerating in 2021-22.

International corn production has expanded 15 percent since 2017-18, fundamentally altering the marketplace.

Where has this growth originated?

Analysis of the three largest global corn producers reveals significant insights, using 2016-17 as the comparison baseline.

Data clearly indicates substantial production increases in Brazil and China beginning in 2021-22. Research published last summer by Dr. Joana Colussi from Purdue University’s Center of Commercial Agriculture examined Brazil’s agricultural expansion.

While the study mentioned China’s growth, the scale became apparent later: China added approximately 4.6 million acres of farmland between 2020 and late 2024 through land reclamation projects and high-quality farmland development.

China’s total cultivated area reached nearly 319.57 million acres in 2024.

What drives this expansion? China’s enormous appetite for pork provides the answer.

Reports from April 2025 showed China maintaining 427 million head of pigs, compared to the European Union’s 132 million head and the United States’ 76 million head during the same period.

This massive livestock population explains their substantial corn requirements for feed production, as well as their soybean needs for protein supplementation in pig feed.

As noted in my Feb. 17 analysis, China’s grain reserves represent almost two-thirds of global ending stocks.

Their food security approach has transformed from rigid government-controlled self-sufficiency (1949-1970s) to market-based strategies emphasizing “absolute security of staple foods.”

Under President Xi Jinping’s leadership, the strategy emphasizes 95 percent grain self-sufficiency, stringent farmland preservation, and agricultural technology advancement, shifting focus from quantity alone to quality and diversification.

Beginning in 2004, policy evolved to prioritize “guaranteed supply” through international commerce while maintaining tight oversight of domestic wheat and rice production.

Consequently, the government maintains a year’s worth of grain reserves, distributing supplies to farmers gradually.

This system also enables government control over farmer pricing.

Given China’s position as the world’s largest grain purchaser, we must analyze President Xi Jinping’s statement about “95 percent grain self-sufficiency, strict farmland protection, and agricultural technology, transitioning from mere quantity to quality and diversification.”

This suggests they have made substantial investments in domestic agricultural expansion and intend to reduce import dependency.

Taking this analysis further, this likely explains their significant investments in Brazilian agriculture to achieve this “self-sufficiency.”

What triggered this strategic shift? Many attribute it to Trump’s trade tariffs. However, examining the timeline reveals Trump’s first presidency spanned 2017-20.

What other major event occurred? COVID-19 was initially identified in China during December 2019, rapidly spreading globally thereafter.

COVID-19 severely damaged global food security by disrupting supply networks, forcing factory shutdowns, and limiting transportation, resulting in widespread hunger and revealing vulnerabilities in food production and distribution systems.

Lockdown measures and economic disruptions amplified these problems, exposing more populations to food insecurity.

The chronology suggests COVID-19 served as the primary catalyst for President Xi Jinping’s strategic thinking shift. If accurate, this altered perspective has transformed the global commodity grain marketplace. This deserves serious consideration!

Returning to U.S. corn utilization completes this analysis. Recent data shows usage patterns for the past two years and projections for the upcoming season.

The information indicates usage has remained relatively stable. As noted, U.S. corn projections for 2026-27 anticipate reduced production, domestic consumption, exports, and ending inventory, which current data confirms.

In conclusion, effective marketing requires understanding both customers and competitors. I detected market changes this past year due to unusually flat price patterns.

This research helps explain the underlying causes. Assuming this data proves accurate, don’t anticipate significant price improvements without major drought conditions.

Additionally, the market appears unable to absorb increased production.

It seems reducing planted acres might support pricing? Is this feasible for producers?

(Note: I research material from Allendale, DTN, USDA, University Land Grants and other credible sources in compiling this article. It is not merely my opinion, but rather a consensus of experts in the trade. Looking for a marketing coach or someone to discuss strategies with? Contact me at [email protected], or call 410-708-8781.)