(Editor’s note: John Hall works as a professional commodities analyst.)

Over the last five weeks, commodities analyst John Hall has been providing farmers with valuable insights to help guide their crop planning for 2026. This week, Hall focuses his attention on worldwide corn supply and demand patterns, drawing from WASDE report data that tracks production figures in million metric tonnes.

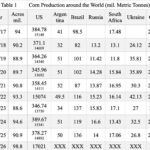

Hall’s first analysis examines global corn production locations, incorporating both U.S. planted acreage and domestic production measured in million bushels.

Several key patterns emerge from the data:

• China holds the position as the world’s second-largest corn producer, utilizing the grain primarily to support their massive swine operations.

• While Argentina’s corn output remains relatively stable, Brazil shows signs of increasing production. However, reports indicate Brazil’s expanding ethanol sector may absorb most of these production gains.

• The situation in Russia and Ukraine presents particular challenges. Military conflict that started in 2014 and intensified in February 2022 has severely impacted their export capabilities, with port facilities becoming strategic targets that disrupted global grain trade.

Moving to domestic consumption patterns, Hall notes that USDA maintains reliable statistics for feed and seed usage, ethanol production, and export volumes, though feed and residual data proves more challenging to track accurately. He cautions against overanalyzing feed usage figures for 2017-18 and 2025-26, describing them as the most reliable estimates currently available.

Categories including food, seed, and ethanol remain relatively steady, while export projections show modest growth for 2025-26. Media reports suggest expanded E15 usage could boost ethanol demand moving forward.

The U.S. Treasury Department has issued updates indicating that usage revisions may emerge from legislative action later this year.

Turning to international export competition, Hall observes that total global exports have remained fairly consistent. With world population growth slowing, increased sales must come at the expense of competitors. The data shows notable gains for the United States in 2024-25.

Hall credits these improvements to successful trade negotiations. “Some of our major trading partners had moved to competitors but the trade deals pulled them back in,” he explains. The analysis reveals how the Russian-Ukraine conflict reduced their export capacity, though the main challenge for U.S. exporters remains transportation costs and shipping distances to those markets.

Examining global corn purchasing patterns, Hall notes that most major buyers maintain friendly relationships with the United States. He believes previous sales losses resulted from higher U.S. prices, but trade agreements have helped recover most of that business.

The discussion concludes with an examination of ending stock levels, presented in both metric tonnes and millions of bushels. Hall includes USDA average pricing data to illustrate the typical relationship where declining stocks correlate with higher prices, while increasing inventories generally lead to lower prices.

China’s stockpiles represent nearly two-thirds of global ending stocks. The nation places extreme importance on food security, given the risks of depending on other countries for essential supplies. Their approach has transformed from rigid government control and self-sufficiency policies (1949-1970s) to market-based strategies emphasizing “absolute security of staple foods.”

Under President Xi Jinping’s leadership, China targets 95-percent grain self-sufficiency while implementing strict farmland protections and advancing agricultural technology. The focus has shifted from simple quantity goals to quality improvements and diversification.

Beginning in 2004, China developed a strategy prioritizing “guaranteed supply” through international trade while maintaining tight control over domestic wheat and rice production. This approach involves government storage of a full year’s grain supply, which is distributed to farmers gradually. This system also enables price control for domestic producers.

Hall acknowledges the complexity of this information, noting his intention to reference this material in future discussions aimed at helping farmers make informed planting choices.

(Note: This analysis draws from research conducted through Allendale, DTN, USDA, University Land Grants and other credible sources. It represents a consensus of trade experts rather than individual opinion. Farmers seeking marketing guidance or strategic consultation can reach Hall at [email protected] or 410-708-8781.)