(Editor’s note: John Hall is a professional commodities analyst.)

Agricultural economists speaking at the Ag Forum Outlook conference held February 19-20 shared projections stating: “The U.S. corn outlook for 2026-27 is for reduced production, domestic use, exports and ending stocks.”

Analysts anticipate the corn harvest will reach 15.8 billion bushels, representing approximately a 7% decrease compared to the previous year.

Farmers are expected to plant corn on 94.0 million acres, which is 4.8 million fewer acres than last year. Yield estimates of 183.0 bushels per acre assume typical planting schedules and average summer weather conditions.

Despite higher beginning inventory levels from the previous year, total corn supplies are predicted to reach 17.9 billion bushels, declining from the record 18.6 billion bushels recorded in 2025-26.

The situation presents a complex picture: planted acreage will decrease, production will drop, but demand is also falling while substantial carryover inventory remains from last year.

Overall U.S. corn consumption for 2026-27 is expected to fall roughly 2% due to reduced domestic consumption and export volumes.

Food, seed, and industrial applications will remain steady at 7 billion bushels. Ethanol production is projected to consume 5.6 billion bushels, based on anticipated stable gasoline consumption and export levels.

Animal feed and residual usage will decline about 3% to 6 billion bushels due to lower available supplies.

Export volumes are forecast to drop by 200 million bushels to 3.1 billion.

America’s share of global corn trade is anticipated to decrease slightly as South American competitors increase exports while worldwide demand growth remains modest.

The global corn landscape has undergone dramatic transformation!

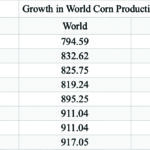

Building on previous analysis from a February 17 column examining corn production worldwide, data using 2017-18 as the baseline year clearly demonstrates that global corn expansion began accelerating in 2021-22.

International corn production has expanded 15% since 2017-18, fundamentally altering market dynamics.

The source of this expansion becomes clear when examining the world’s three largest corn producers, using 2016-17 as the comparison year.

Data reveals substantial production increases in Brazil and China beginning in 2021-22. Research by Dr. Joana Colussi at Purdue University’s Center of Commercial Agriculture highlighted Brazil’s expansion last summer.

While China’s growth received less attention initially, the country has added approximately 4.6 million acres of farmland between 2020 and late 2024 through land reclamation projects and high-quality agricultural development initiatives.

China’s total cultivated area reached nearly 319.57 million acres in 2024.

This expansion stems from China’s massive pork consumption. The numbers are staggering.

Reports from April 2025 indicated China maintained 427 million head of pigs, compared to the European Union’s 132 million head and the United States’ 76 million head during the same period.

This enormous swine population explains China’s corn requirements for feed production and their soybean needs for protein supplementation in pig feed.

As noted in the February 17 analysis, China’s ending grain stocks represent nearly two-thirds of global ending stocks.

China’s food security approach has evolved from rigid state-controlled self-sufficiency during 1949-1970s to a market-based strategy emphasizing “absolute security of staple foods.”

Under President Xi Jinping’s leadership, the strategy targets 95% grain self-sufficiency, stringent farmland preservation, and agricultural technology advancement, shifting focus from quantity alone to quality and diversification.

Beginning in 2004, the strategy adapted to prioritize “guaranteed supply” through international trade while maintaining tight control over domestic wheat and rice production.

Consequently, the government maintains a year’s grain supply in storage, releasing it to farmers gradually.

This system also enables government control over farmer pricing.

Given China’s position as the world’s largest grain purchaser, President Xi Jinping’s statement requires careful analysis: “95 percent grain self-sufficiency, strict farmland protection, and agricultural technology, transitioning from mere quantity to quality and diversification.”

This suggests significant investment in domestic agricultural expansion aimed at reducing import dependency.

This strategy likely explains China’s substantial investments in Brazilian agriculture to achieve this “self-sufficiency.”

What triggered this strategic shift? Many attribute it to Trump administration tariffs. However, examining the timeline reveals Trump’s first presidency spanned 2017-20.

Another significant event occurred: COVID-19 was initially identified in China during December 2019, rapidly spreading globally.

COVID-19 severely impacted global food security by disrupting supply chains, forcing factory shutdowns, and restricting transportation, resulting in widespread hunger and exposing vulnerabilities in food production and distribution systems.

Lockdowns and economic disruptions amplified these challenges, increasing food crisis exposure for millions.

The timeline suggests COVID-19 served as the primary catalyst for President Xi Jinping’s strategic mindset shift. If accurate, this changed perspective has transformed the global commodity grain marketplace. This deserves serious consideration!

Returning to U.S. corn consumption data completes this analysis. Recent figures show usage patterns for the past two years and projections for the upcoming year.

These numbers indicate usage has remained relatively stable. As noted, U.S. corn projections for 2026-27 anticipate reduced production, domestic consumption, exports, and ending stocks, which current data supports.

In conclusion, effective marketing requires understanding both customers and competition. Market flatness over the past year suggested fundamental changes were occurring.

This research helps explain the underlying causes. Assuming this data proves accurate, significant price improvements seem unlikely without major drought conditions.

Additionally, markets appear unable to absorb increased production.

Reducing planted acreage could potentially support prices. Is this a viable option for farmers?

(Note: Research material compiled from Allendale, DTN, USDA, University Land Grants and other credible sources. This represents expert consensus rather than individual opinion. For marketing coaching or strategy discussions, contact [email protected] or call 410-708-8781.)